Are you a committed employer? Continuously seeking meaningful ways to support your workforce?

Providing child care support for employees is becoming an increasingly valuable way to support your team.

The good news is that both Federal, New York State* and New York City programs offer tax credits to help cover your employees’ child care costs.

Before getting into all the details of the program, you may review the M Kohn & Co Practical Advice and Quick Summary:

Focus on 3 Core Considerations: Your cash flow (plan expenditures carefully to maximize the credit while maintaining liquidity), stay informed of Proposed Legislation (changes to the NY credit may increase to 100 %), and ensure your employees understand that the benefits may be taxable.

When employers proactively manage expenses, monitor legislative updates, and communicate clearly with employees, they can maximize the value of childcare tax credits.

Detailed overview of the federal credits:

Federal Employer-Provided Child Care Credit (IRC § 45F)

The federal Employer-Provided Child Care Credit, (Internal Revenue Code Section 45F), is a general business credit available to employers who incur qualified childcare costs for the benefit of their employees.

How the Credit Works:

- You can claim:

- 40% (or 50% for eligible small businesses) of qualified childcare expenses

- 10% of qualified child care resource and referral costs.

- The maximum annual credit is $500,000 (or $600,000 for eligible small businesses).

- For tax years beginning after 2026, these limits are adjusted for inflation.

Qualified Expenses:

- Qualified child care facility costs include costs to acquire, construct, rehabilitate, or expand its property.

- Operating costs include employee training, scholarships, increased compensation for trained staff, and payments under contract with a qualified child care facility or intermediary.

- Qualified child care resource and referral expenses are amounts paid under contract to provide child care resource and referral services to employees.

Qualified Child Care Facility Requirements:

- The facility’s principal use must be to provide child care assistance.

- It must comply with all state/local laws and licensing.

- Enrollment must be open to employees.

- If the facility is the taxpayer’s principal business, at least 30% of enrollees must be dependents of employees.

- The facility cannot discriminate in favor of highly compensated employees.

- When contracting with an outside provider, the facility must comply with all state/local laws and licensing.

Recapture Provisions:

- If the facility ceases to operate as a qualified child care facility or is sold (without the buyer assuming recapture liability), a portion of the credit may need to be repaid, based on how long the facility was in service.

No Double Benefit:

- The basis of property for depreciation must be reduced by the amount of the credit.

- No other deduction or credit is allowed for the same expenditures.

How to Claim:

- Employers claim the credit using IRS Form 8882.

Below is a brief overview of the New York State credit available:

New York State Employer-Provided Child Care Credit

New York State offers its own employer-provided childcare credit, which is designed to supplement the federal credit and further encourage businesses to support childcare for employees.

Eligibility:

- Available to taxpayers subject to NYS corporate, personal, or franchise taxes who qualify the federal credit for:

- Qualified expenses for a childcare facility located in New York State, or

- Qualified childcare resource and referral expenses for employees working in New York State.

Credit Amount:

- For tax years beginning on or after January 1, 2022, the NYS credit equals 200% of the federal credit (IRC § 45F) for qualifying NYS expenditures.

- As of 2026, this means the NYS credit is effectively 100% of qualified childcare facility expenditures plus 20% of qualified child care resource and referral expenditures paid or incurred during the tax year.

- The NYS credit is capped at $500,000 per tax year, applied at the entity level.

Refundability:

- The NYS credit is refundable, meaning if the credit exceeds the taxpayer’s tax liability, the excess is refunded.

Recapture:

- If the federal credit is recaptured due to a closure of operation or change in ownership of a NYS facility, the NYS credit must also be recaptured, but only up to the amount of the NYS credit originally allowed.

How to Claim:

- Corporations use Form CT-652; other taxpayers use Form IT-652.

Key Insights:

- Federal and NYS credits can be claimed together for the same expenditures, but NYS specifically enhances the benefit for facilities and services in New York.

- Strict requirements apply to what constitutes a qualified facility and eligible expenditures.

- Recapture rules can require repayment of credits if the facility stops qualifying within a certain period.

- NYS credit is refundable and more generous than the federal credit for qualifying NYS expenditures.

If you’re considering offering childcare support or want to understand how these credits apply to your business, our team can help you evaluate the opportunity and ensure proper compliance. Reach out, we'll be glad to help.

For a better understanding of how employer-provided childcare benefits may impact employees, see our related article covering the employee perspective.

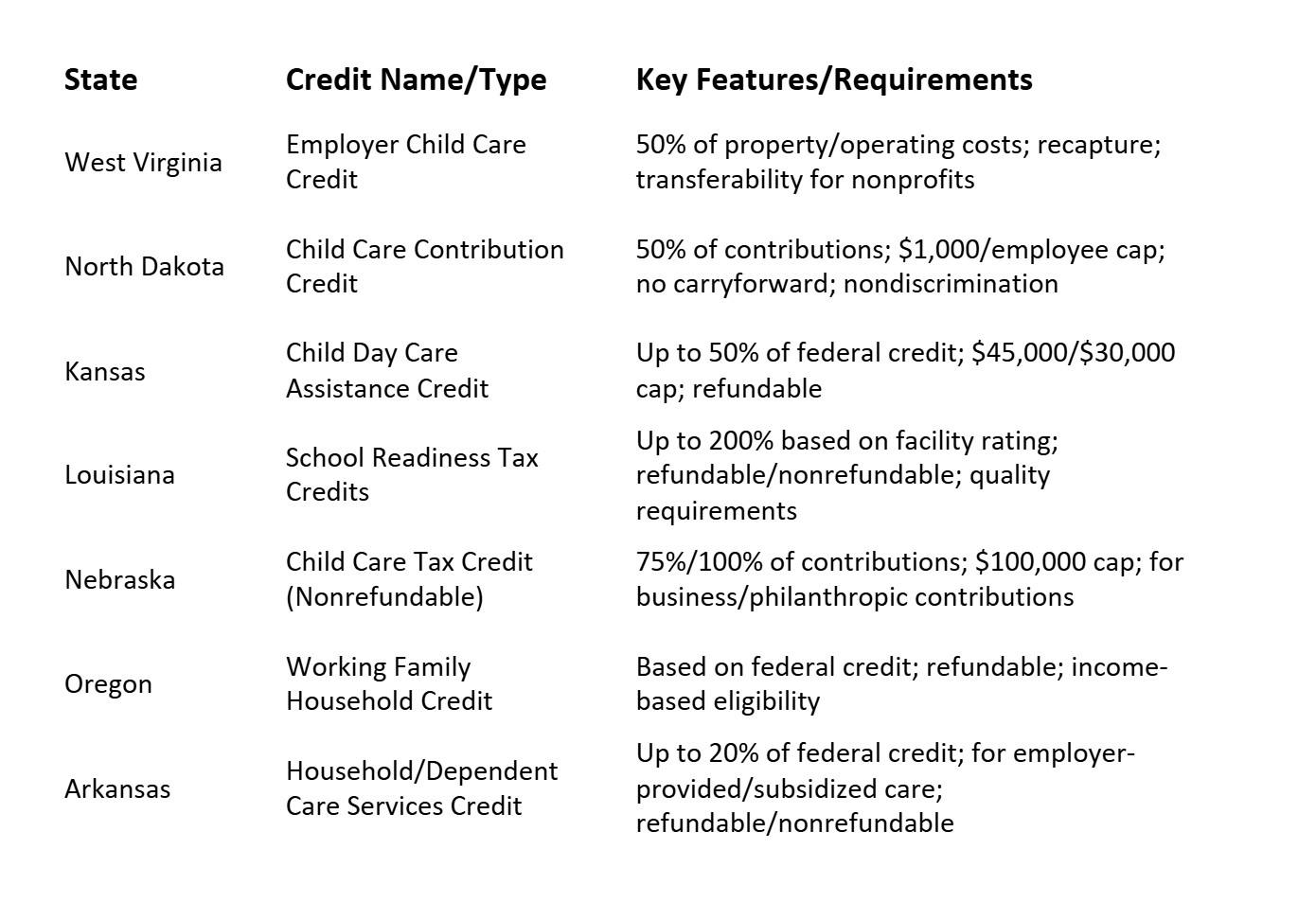

*New York State credit amounts and structure are subject to legislative updates. See the comparison of other state programs below.