Child Care Tax Credits: Federal and New York State

- Impact on Employees’ Taxes:

Employer-sponsored child care is becoming more common as businesses look for meaningful ways to support their employees.

While these benefits can reduce out-of-pocket childcare costs, it is important for employees to understand how they are treated for tax purposes and how they may impact overall tax liability.

The good news is that both Federal, New York State* and New York City programs offer tax credits to your employer to help cover your child care costs.

To understand how these programs benefit employers, see our related article here → Employer Blog

Employer-Sponsored Child Care is a valuable benefit, but employees need to understand how it affects their taxes.

1. Federal Tax Treatment of Employer-Sponsored Child Care

A. Exclusion from Income: Dependent Care Assistance Programs (IRC § 129)

- Employees can exclude from their gross income up to $7,500 per year ($3,750 if married filing separately) of employer-provided dependent care assistance for 2026 and later years. This is an increase from the previous $5,000 limit.

- Qualifying Benefits: The exclusion applies to benefits provided under a written Dependent Care Assistance Program (DCAP), which may include:

- Direct payments to a childcare provider

- Reimbursement to the employee for qualified expenses

- On-site employer-sponsored childcare facilities

- Contributions to a dependent care flexible spending account (FSA).

- Qualified Expenses:

- Child under age 13

- dependent/spouse incapable of self-care

- must enable the employee (and spouse, if married) to work or look for work

- Earned Income Limitation: The exclusion cannot exceed the lesser of the employee’s or (if married) the spouse’s earned income for the year.

- Non-Discrimination: The plan must not discriminate in favor of highly compensated employees [1].

B. Taxability of Excess Benefits

- Amounts above the $7,500 limit (or $3,750 if married filing separately) are taxable and must be included in the employee’s gross income.

C. Reporting Requirements

- Form W-2, Box 10: Employers must report the total amount of dependent care benefits provided to the employee in Box 10 of Form W-2, regardless of whether the amount is excludable or taxable.

- Taxable Portion: Any amount exceeding the exclusion limit is also included in Boxes 1, 3, and 5 (wages subject to income tax, Social Security, and Medicare).

D. Interaction with the Child and Dependent Care Credit (IRC § 21)

- No Double Benefit: Employees cannot claim the child and dependent care tax credit for expenses paid with employer-provided benefits that are excluded from income. Only unreimbursed, out-of-pocket expenses above the excluded amount may be used to claim the credit.

E. On-Site Child Care Facilities

- The fair market value of care provided at an employer’s on-site facility can be excluded from income if the facility qualifies under the DCAP rules and the value does not exceed the annual exclusion limit.

2. New York State Tax Treatment

A. State Income Tax Exclusion

- Conformity with Federal Law: New York State generally follows the federal exclusion for employer-provided dependent care assistance. Amounts excluded from federal income are also excluded from New York State income.

B. Additional State Credits

- NYS Employer-Provided Child Care Credit: This credit is claimed by employers, not employees, but it encourages more employers to offer childcare benefits.

- NYS Child and Dependent Care Credit: Employees may also be eligible for the New York State child and dependent care credit for unreimbursed expenses, similar to the federal credit, but only for amounts not excluded from income under a DCAP.

C. Practical Example

- Mr. Smith’s employer provides $8,000 in dependent care benefits through a DCAP in 2026. Mr. Smith is married and files jointly.

- Federal Exclusion: Mr. Smith can exclude $7,500 from his income. The remaining $500 is taxable and reported as wages.

- W-2 Reporting: His W-2 will show $8,000 in Box 10. The $500 excess will also be included in Boxes 1, 3, and 5.

- Tax Credit: Mr. Smith cannot claim the federal or NYS child and dependent care credit for the $7,500 excluded, but may claim the credit for any additional, unreimbursed qualifying expenses above that amount.

Key Insights:

- Most employer-sponsored childcare benefits are excluded from income up to $7,500 per year (2026).

- Amounts above the limit are taxable.

- Employers must report all dependent care benefits on Form W-2, Box 10.

- Excluded benefits cannot be used to claim the child and dependent care credit.

- New York State generally follows federal rules for income exclusion and offers additional credits for unreimbursed expenses.

If you receive employer-sponsored child care benefits or are considering participating in a dependent care program, it is important to understand how these benefits impact your taxable income and available credits. Our team can help you review your situation and ensure you are maximizing available benefits while staying compliant.

For a full overview of how these programs work from the employer side, including available credits and planning considerations, see our related article here

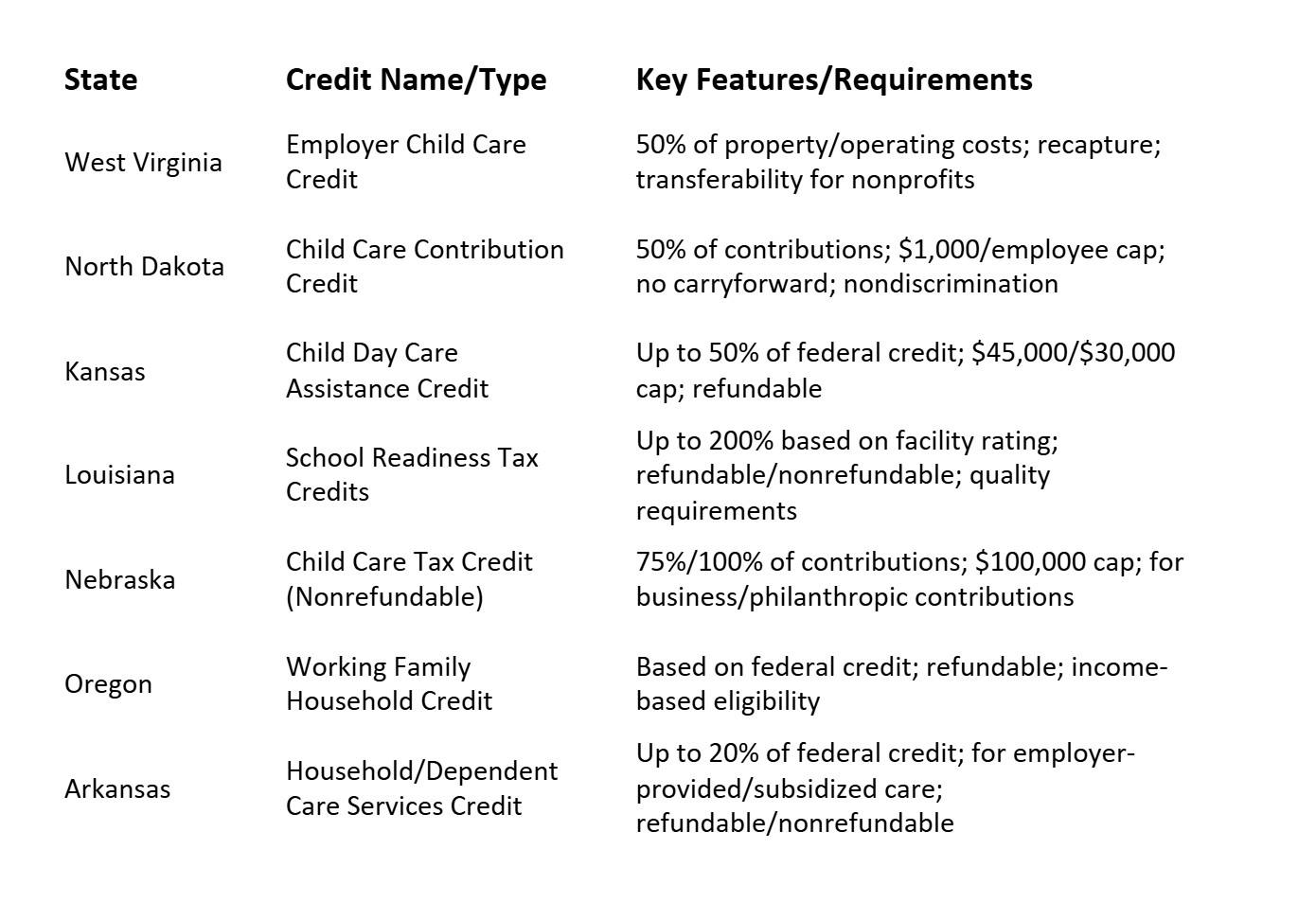

*New York State credit amounts and structure are subject to legislative updates. See the comparison of other state programs below.